- By tabacco_Admin

- Brand Charcha

- May 21, 2026

Rajasthan High Court’s Hammer on Arbitrary Duty Collection Based on Hypothetical Production Capacity Could Prove a Turning Point Not Just Legally, But for the Future of the Entire Industry

A recent interim order by the Rajasthan High Court has once again brought the tobacco and pan masala industry to the center of policy debate. The judgment is expected to have far-reaching implications. The Hon’ble High Court has granted interim relief to a firm challenging the new capacity-based excise duty regime on pan masala packing machines, implemented from 1 February 2026.

A petition filed before the High Court challenged the current system of levying excise duty on packing machines used in tobacco and pan masala manufacturing. The Court has issued notices to the Central Government and related departments on the plea challenging arbitrary tax collection based on hypothetical production capacity. This case could prove to be a major turning point, not just legally, but for the future of the industry as a whole.

The petition was filed by Vinayak K., partner of Trimurti Leaves, located in Mandore Industrial Area, Jodhpur, challenging the new machine-capacity-based tax system as unconstitutional. The plea argued that instead of actual production, excise duty and related levies, including GST and other cesses of up to 40 percent, are being determined on the basis of a machine’s estimated or notional production capacity.

Counsel for the petitioner argued that machines do not operate at full capacity continuously, making the system unreasonable. After preliminary hearing, the High Court granted interim relief and sought responses from the Central Government and Revenue Department.

At present, excise duty on tobacco and pan masala manufacturing units is determined on the basis of machine production capacity. In other words, tax is assessed on what a machine can theoretically produce, even if actual output is significantly lower. Industry experts argue this system is impractical. The industry’s objection is that taxation should be based on reality, not theoretical capacity, because full utilization of machine capacity is rarely possible.

Factors such as market demand, raw material availability and operating costs all affect production. Yet under machine-based taxation, manufacturers are required to pay tax on full capacity even when actual output is lower. This has had a direct impact, particularly on small and medium manufacturers, becoming an additional financial burden.

The petition also argues that this system violates the right to equality under Article 14, as applying uniform tax treatment to units operating under vastly different circumstances cannot be considered just. Once the Centre and Revenue Department respond, an important question before the Court will be whether taxation should be based on actual production or potential capacity.

This is not merely a tax dispute, but a test of policy balance. On one hand, the government seeks revenue protection and transparency; on the other, industry demands practicality and fairness. With high tax rates, a stringent regulatory framework and rising raw material costs, the tobacco and pan masala industry is already facing multiple challenges. In that context, the High Court’s interim relief has brought a much-needed sense of optimism.

The hearing in Rajasthan High Court will determine whether the capacity-based tax regime will continue or be shifted to a production-based model. If the Court rules in favour of industry, it could bring major relief to tobacco and pan masala manufacturers across India. If the present system is upheld, the industry will have to balance operations within this framework.

The forthcoming judgment may determine the direction in which India’s tobacco and pan masala industry moves forward—towards estimated capacity or actual production. Clearly, the industry is currently passing through a crucial transition. The Health and National Security Cess, RSP-based taxation, and compounded levy structure have completely altered the industry’s cost structure.

While the government’s revenue collection targets are aggressive, the industry is struggling to balance profitability, volume and compliance. The new tax system has placed the sector in a classic “between a rock and a hard place” situation. Manufacturers are uncertain how to navigate it. Raising prices risks losing consumers, while reducing quantity risks consumer dissatisfaction.

As a result, intense deliberation is underway within the industry around weight and MRP management. During regular market surveys, Tobacco Plus found the situation deeply concerning. Even two months after implementation of the new taxation system, factories are not operating at full production, leading to shortages of multiple brands in the market. Continuous discussions are underway on how to manage MRP and pouch quantity while accommodating higher taxes and protecting consumer affordability.

The new tax structure has become especially concerning for small and medium manufacturers, whose production capacity is limited but whose tax liability is determined on standardized machine capacity. While the government’s objective may be to curb tax evasion and secure revenue, the industry sees the structure as excessively rigid and impractical.

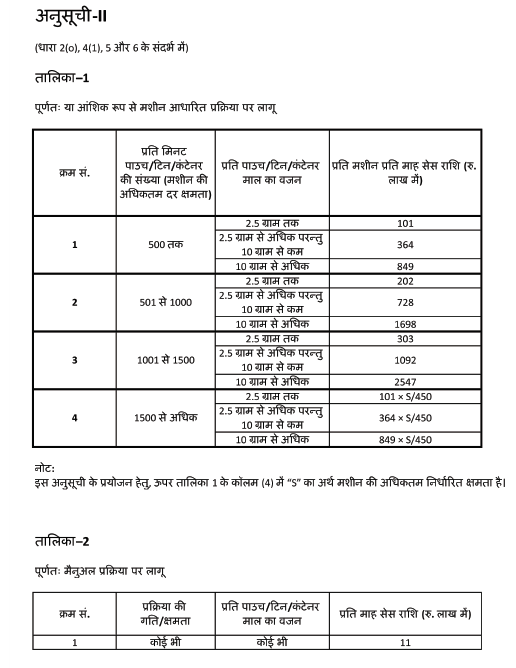

This difficult situation has emerged because tax determination has been linked to packing machine speed, pouch weight, and declared retail sale price. In fact, machine standard speed has been fixed according to pouch weight. If pouch weight is up to 2.5 grams, machine speed is deemed 500 pouches per minute. But once pouch weight exceeds 2.5 grams, the standard speed is assumed to jump to 1,000 pouches per minute, regardless of actual output.

This provision has emerged as the industry’s biggest concern. A marginal increase in weight doubling tax liability could destabilize many units financially. Technically, machines cannot continuously run at 1,000 pouches per minute, yet taxation has been based on this assumption.

Under the new system, a machine producing pouches up to 2.5 grams at 500 pouches per minute attracts an annual cess of approximately ₹101 lakh. But once pouch weight exceeds 2.5 grams and machine speed is deemed to rise to 1,000 pouches per minute, cess jumps directly to ₹202 lakh.

In other words, if manufacturers increase quantity or production capacity, cess burden escalates sharply in the same proportion. A third major factor is MRP-based taxation—if MRP rises, tax automatically increases.

This leaves the industry with little room to either increase weight or raise prices. Since the new tax system came into force on 1 February, the pan masala and smokeless tobacco industry has been caught in deep uncertainty. It would be fair to say the industry is currently being squeezed between weight, machine capacity, and MRP.

There is, however, another side to this. The new tax structure may effectively put a brake on the long-running quantity and price war in pan masala. In simple terms, the market may now move from a quantity war to a quality war. Tobacco Plus believes this phase will be challenging for smaller brands driven by aggressive pricing and grammage strategies, while premium and quality-focused brands may emerge stronger.

The legal basis of the new tax system lies in notifications issued under Section 4A of the Central Excise Act, 1944, the Central Goods and Services Tax Act, 2017, and the Health Security and National Security Cess Act, 2025. Under these provisions, pan masala and tobacco products have been treated as specified goods, subject to special valuation and cess.

Under Section 4A, pan masala was already under MRP-based valuation, where tax is calculated after a prescribed abatement of around 55 percent on declared MRP. Under the new regime, machine-based cess has now been effectively superimposed on this framework. This is precisely the provision industry sees as most problematic.

A minor increase in pouch weight leading to a doubling of tax liability could seriously damage the financial health of small and medium manufacturers. Machines technically cannot sustain 1,000 pouches per minute continuously, yet taxation has been structured on this assumption.

In this backdrop, the High Court’s decision is extremely significant for the industry, as it opens the door to challenging this arbitrary tax mechanism. The next hearing is scheduled for 13 July 2026, which means the voice raised from Jodhpur may well prove consequential for the entire industry.